share on

Many happy returns! With Hong Kong’s MPF Scheme just about to turn 20, how can HR pull the right levers to provide the best possible deal for employees? Robert Blain reports.

When Hong Kong’s Mandatory Provident Scheme (MPF) was launched in December 2000, it was considered little more than a legal obligation by HR managers. A time-consuming nuisance.

But now – two decade on – the retirement scheme landscape has now changed. The MPF now boasts 4.3 million members. The average sum for Hong Kong employees now tops HK$220K and the scheme has just ticked above HK$1 trillion in August. No longer just an annoying piece of paperwork that has to be dealt with, MPF is now a significant plank in any competitive employee benefits package.

But given the ever-increasing financial clout of the scheme, how can HR choose the best MPF provider for its organisation? And how can it pull the right levers to provide a scheme that gives the best possible returns but ticks all the right boxes for employees?

While a healthy return on investment is obviously an important factor when considering an MPF provider, a successful is more nuanced than that. Flexibility, voluntary top-ups, tax offsets and additional employer contributions are all factors that can sweeten the pot when trying to attract, and keep, talent at our organisation.

“Organisations should shop around because it shows employers are thinking of their staff. More employers are using MPF as an employee benefit, not an obligation.”

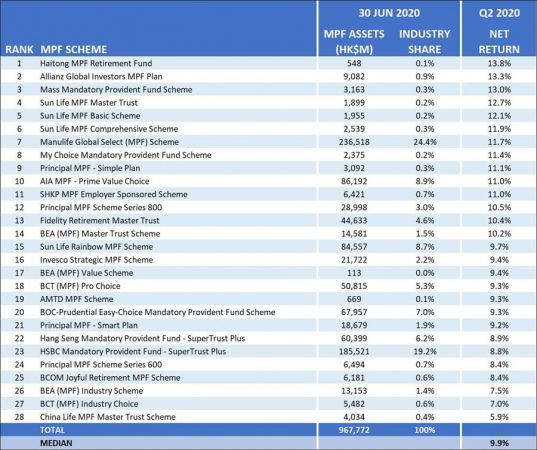

Dollars and sense

Financial returns are, of course, one of the first considerations of an MPF scheme (refer to MPF returns table below) but it would be a misguided to focus purely on this one aspect. Increasingly, it is incumbent upon HR to take a closer look.

“Employers should look around. The average MPF account balance is now over $220k – not a small amount – so the chances are employees are now monitoring their MPF,” Francis Chung, president of MPF Ratings told Human Resources.

“When MPF commenced it was exclusively employer driven, but with the introduction of employee choice arrangements in 2012, the introduction of tax voluntary contributions in 2019, and rising account balances, employees are now empowered to make decisions for their own MPF accounts,” Chung said.

Another good reason for organisations to shop around is because it shows employers are thinking of their staff. More employers are using MPF as an employee benefit, not an obligation.

“Forty-five percent of the respondents to the MPF Expectations Survey said they were providing additional voluntary contributions to staff. If (HR) is using MPF as a benefit then it makes sense to maximise the benefit by finding the most suitable scheme for staff,” he added.

However as Ross Hui, VP and head of compensation and benefits for Asia Pacific at Moody’s Corporation points out, it’s an area HR can do more for employees, and an initiative his organisation actively embraces – along with a number of other rewards.

“We have introduced various measures in promoting financial wellness including partnering with the MPF provider for regular seminar and briefing sessions as well as introducing those tax efficient retirement measures to facilitate the financial wellness of our employees,” Hui told Human Resources.

Source: MPF Ratings

It’s easy to fall into the trap of taking an approach to MPF based solely on fees and performance. But a suitable MPF scheme is multi-faceted and it’s well worth investing a little time to ensure a plan that’s right for your organisation.

“Being fee competitive is important, but performance is something that MPF schemes don’t control. What they can control however are aspects such as administration efficiency, services to members, educating members and ensuring a good selection of funds,” Chung explained.

Hui concurs, adding that “employers should not be too obsessed with financial return as the sole yardstick to evaluate its MPF provider”.

“Apart from the financial performance, employer should also consider the fund choices in terms of variety, fund charges, customer service level, user interface friendliness as well as financial wellness education to enable an all-rounded assessment of the MPF provider,” Hui said.

“In short, one should look at the value-for-money proposition of the whole scheme, not just performance and fees,” added Chung.

Spoiled for choice?

There is a fairly wide range of MPF providers available in Hong Kong but choosing one can be bewildering. Finding the best plan for your employees is a decision that should not be taken lightly. In addition, the provider that felt right 20 years ago when MPF started might no longer be suitable for your charges. But it’s advisable to look before you leap.

“The employer should establish a set of criteria to evaluate its MPF vendor but should not be biased by short-term investment return to make a swap decision casually,” said Hui.

Bringing in dual or multiple MPF providers which supplement with each other is another option worth considering – enabling employees to select the MPF schemes which best fits their needs.”

Another bugbear for many employees in Hong Kong is the need to change MPF providers when they change jobs. Consolidating funds can be a time-consuming and messy process.

“The Employee Choice Arrangement (launched in November 2012) is a potential way out of this challenge. Employees can take the lead to consolidate their existing employee account into one single MPF vendor, despite the process having to be employee self-initiated,” said Hui.

HR can also help smooth the way during the onboarding process.

“HR can incorporate a consolidation checking process as part of the standard onboarding logistics to facilitate employees to work on their MPF account consolidations if needed.”

“45% of respondents to the MPF Expectations Survey said they were providing additional voluntary contributions to staff.”

Tailored approach

Any provider worth its salt should also be a good source of information.

“MPF is a key pillar of Hong Kong people’s retirement savings, making it important to weigh all factors when deciding on a service provider. Fund performance, fees and charges must of course be considered as they have an impact on the net return of a fund,” said Elaine Lau, chief corporate solutions officer at AIA for Hong Kong and Macau.

Lau added that digital services have become more essential than ever before and raises a number of important questions for HR. Can MPF assets and accounts be consolidated online? How adequate is the investment information available online? Considerations like the number of benefit statements or fund fact sheets offered are less obvious but may be more critical.

“A caring HR manager should also consider the range and quality of services provided. Responsive, tailored support – for example, different support for different life stages – is tremendously valuable, Lau added.

There’s no need for HR to be daunted, and bogged down in the detail. Selecting MPF funds needn’t be as difficult or complicated as it seems, observed Lau.

That said, employees are often confused about what choices are available to them and how to select the best mix of funds.

Lau suggested that HR can take a proactive role and remind employees to review their MPF investment portfolio regularly, to ensure it remains in line with their investment objectives, preferred asset allocation and risk tolerance level.

“In general, it’s good practice to conduct a portfolio review once every six months to a year. A review should also be undertaken when entering a new life stage for example, getting married or having a child – to allow for timely adjustments to the portfolio where needed,” added Lau.

Adapting MPF during challenging times

“Given the outbreak of COVID-19, many employer clients are adapting a work-from-home arrangement,” said Rainbow Pan, general manager for Wealth and Pensions at Sun Life Hong Kong.

To combat the inconvenience Pan advised arranged online support to employers such as investment webinar to their employees and keeping abreast of the latest market trend under the fluctuating investment market is also prudent, as well conducting “regular online meeting with employer clients to ensure all MPF administrative works are running as usual during the period”.

A digital approach can also pay dividends. Pan suggests that by organising segmented investment webinars, providers can effectively communicate with members on their respective investment objectives and provide appropriate insights useful at different stages of an employee’s life.

For employee ease of keeping up to date on their MPF, a provider that has app capability is also a plus. A surprising number of MPF providers still don’t have this feature.

“We are going to launch a mobile app to clients in late 2020,” said Pan, “giving clients

more tools to manage their MPF at any time.”

Although in some regards MPF is one aspect of employee benefits that remains business-as-usual during the pandemic, sound investment principles still apply.

“Other than returns, service is the second most important factor to consider,” said Pan.

“MPF providers should provide employers and employees with perfect tools for MPF management in an efficient way like arranging digital access of MPF accounts and carry out MPF management like fund switching,” she added.

“Traditional thinking tends to be “big is better”, observed Chung from MPF Ratings.

“But the data we published in July would suggest otherwise. What I would say though is again employers and employees need to look at the broader picture.

“Some of the smaller schemes are delivering better performance, but do they have a broad range of fund choice suitable to all employees of a company? Do they offer efficient services and do they provide the type of engagement with employees which the bigger schemes can do with better resources? All these things need to be considered,” Chung concluded.

share on

Follow us on Telegram and on Instagram @humanresourcesonline for all the latest HR and manpower news from around the region!

Related topics